Receiving a collection notice can be stressful and overwhelming, especially when you're unsure about the debt's legitimacy or details. Many consumers don't realize they have powerful legal rights when dealing with debt collectors, including the right to request proof that a debt is actually yours. A debt validation letter serves as your first and most important step in protecting yourself from errors, fraud, and unfair collection practices.

What Is a Debt Validation Letter?

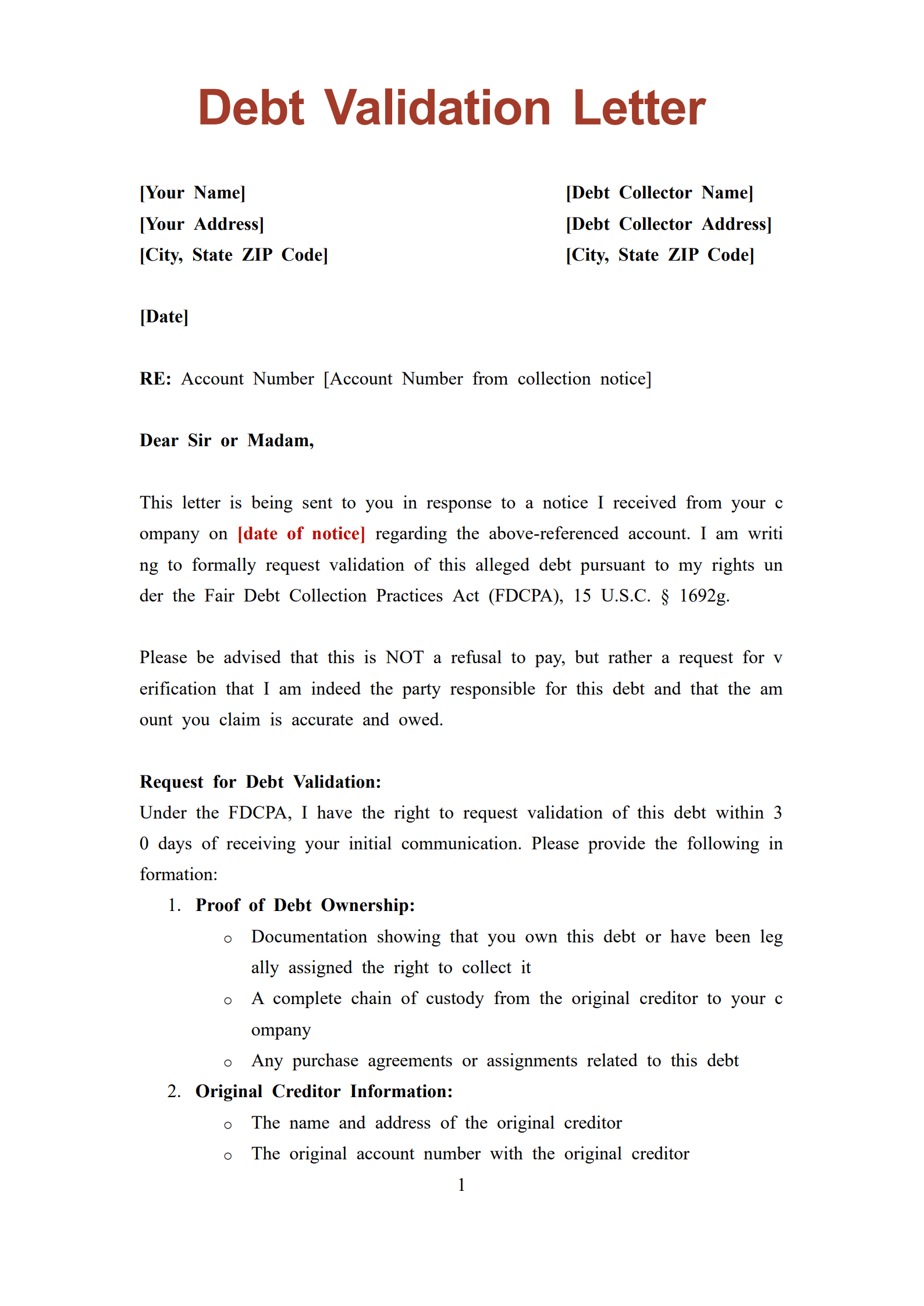

A debt validation letter is a formal written request sent to a collection agency demanding they provide proof that you legitimately owe the debt they're attempting to collect. This legal document, protected under the Fair Debt Collection Practices Act (FDCPA), requires collectors to verify the debt's accuracy and their legal right to collect it before continuing their collection efforts.

When you send a debt validation letter, you're essentially saying "prove it" to the collection agency. The letter requests specific documentation including the original creditor's name, the amount owed, itemization of charges, proof of the collector's license to operate in your state, and evidence that the debt is within the statute of limitations.

The debt validation letter must be sent within 30 days of receiving the initial collection notice. During this window, debt collectors are legally required to cease collection activities until they provide adequate validation. This pause gives you breathing room to assess the situation and determine your next steps.

Unlike disputing a debt with credit bureaus, a debt validation letter goes directly to the collection agency itself. This distinction matters because you're addressing the source of the collection attempt rather than just questioning its appearance on your credit report.

Why Send a Letter of Debt Validation?

Using a debt validation letter provides numerous advantages that can protect your financial interests and legal rights.

Prevents Identity Theft and Fraud

Collection agencies sometimes pursue debts that don't belong to you due to identity theft, mixed files, or simple clerical errors. A debt validation letter forces the collector to prove the debt is legitimately yours before you make any payment or acknowledgment that could reset the statute of limitations.

Confirms Debt Accuracy

Even if a debt is yours, the amount claimed might be inflated with improper fees, incorrect interest calculations, or charges that weren't part of the original agreement. The debt validation letter requires collectors to provide a detailed breakdown, allowing you to spot and challenge discrepancies.

Establishes Legal Protection

Sending a debt validation letter creates a paper trail proving you've exercised your rights under the FDCPA. If the collector continues aggressive tactics without providing proper validation, they may be violating federal law, which could give you grounds for legal action.

Buys Time to Assess Options

The validation period halts collection activities, giving you time to review your financial situation, consult with legal counsel if needed, and develop a strategic response without the pressure of constant collection calls and letters.

Filters Out Zombie Debts

Some collection agencies purchase old debts for pennies on the dollar and attempt to collect on debts that are past the statute of limitations or have already been discharged in bankruptcy. A debt validation letter can expose these "zombie debts" that you may no longer have legal obligation to pay.

Essential Elements of an Effective Debt Validation Letter

Your debt validation letter should include specific components to maximize its legal effectiveness and improve your chances of receiving proper documentation.

Begin with your complete contact information, including full legal name and current mailing address. Reference the collection agency's correspondence by including the date of their initial collection letter and any account or reference numbers they provided.

Clearly state that you're requesting validation of the debt under Section 809(b) of the Fair Debt Collection Practices Act. This legal citation puts the collector on notice that you understand your rights and expect compliance with federal law.

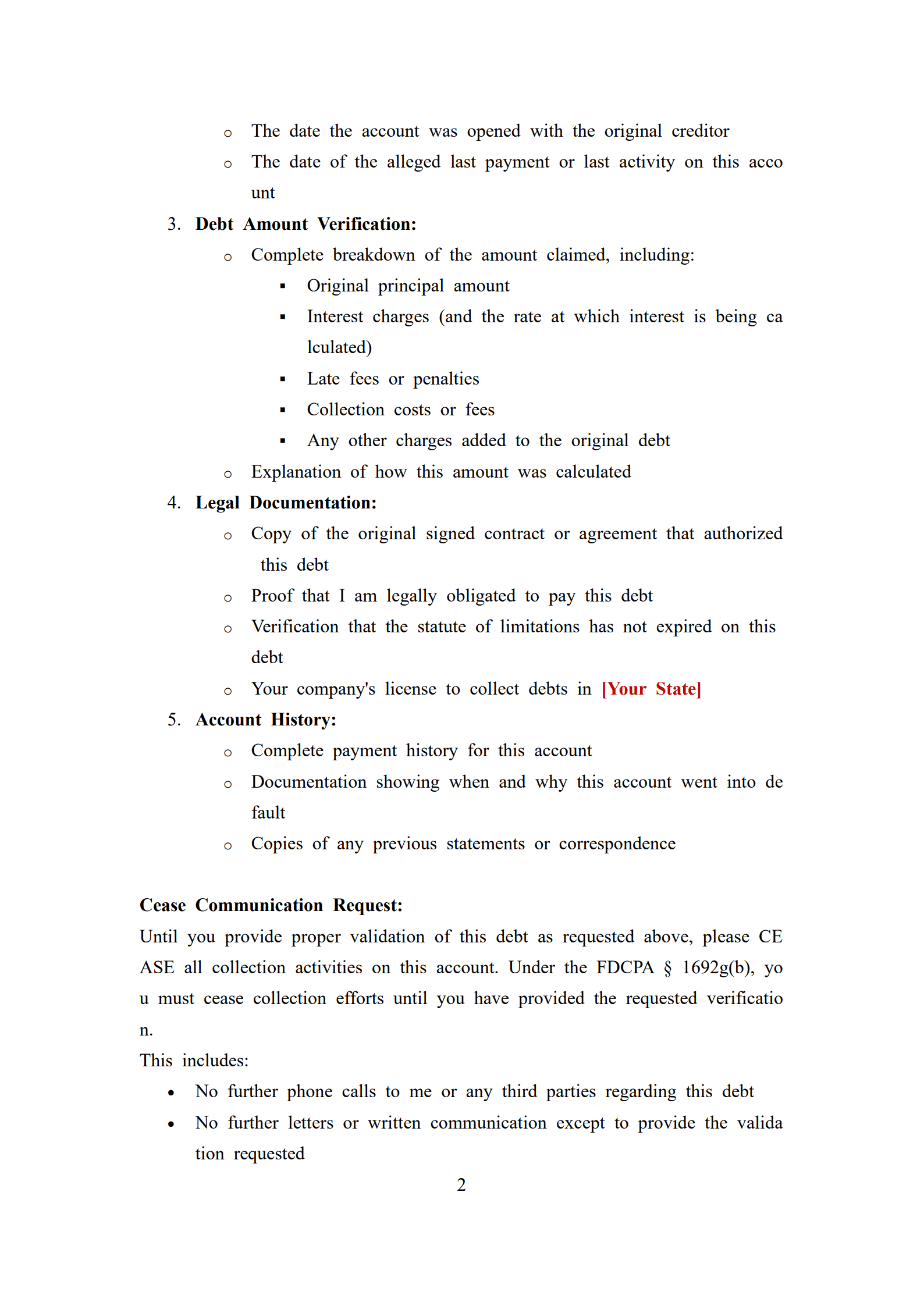

Demand specific documentation in your debt validation letter, including proof that the collection agency owns the debt or has been authorized to collect it, the name and address of the original creditor, a copy of the original signed contract or agreement establishing your obligation, an itemized accounting of the debt showing the original balance and any added fees or interest, and verification that the debt is within your state's statute of limitations.

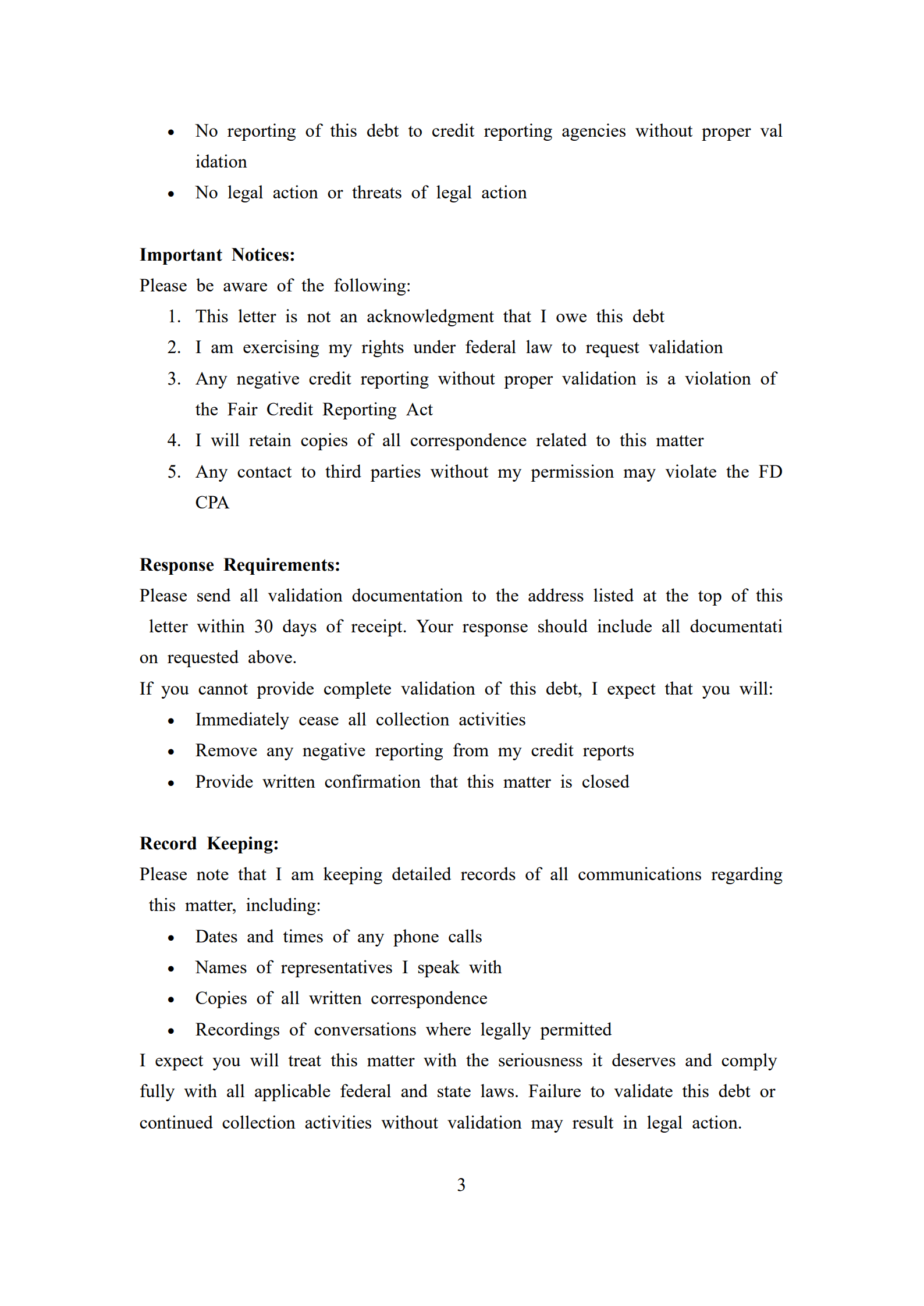

Request that all collection activities cease until proper validation is provided. Explicitly state that you're exercising your right to dispute the debt and that any continued collection attempts without validation constitute harassment under the FDCPA.

Include language prohibiting the collector from reporting the debt to credit bureaus until they've provided validation. Also specify that you want all future communications in writing only, which prevents aggressive phone call tactics.

Tips for Maximizing Your Debt Validation Letter Impact

Strategic approaches can strengthen your debt validation letter and improve outcomes.

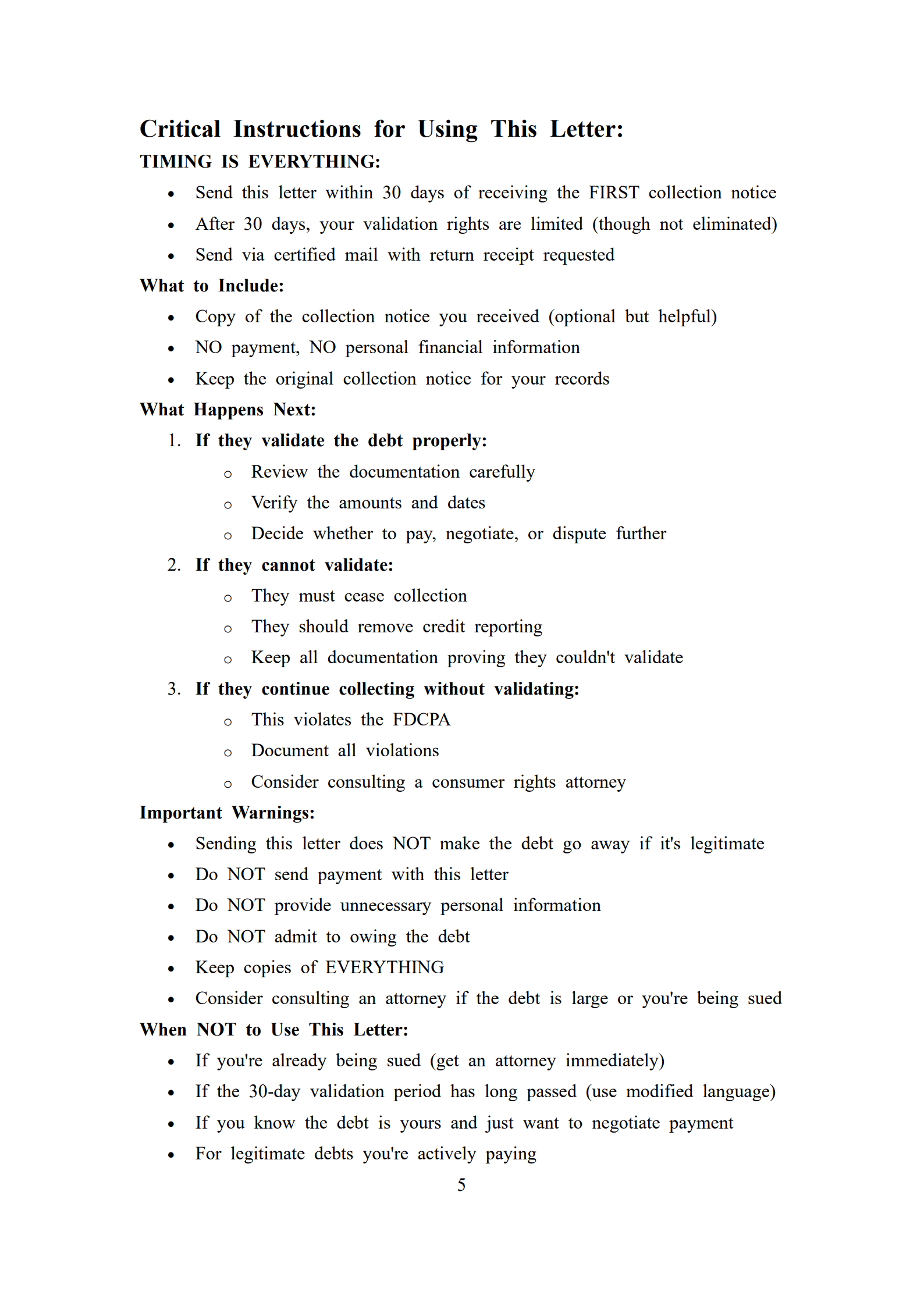

Act Within the 30-Day Window

The most critical tip is timing. Mail your debt validation letter within 30 days of receiving the collection agency's initial notice. While you can still send a validation request after this window, the collector isn't legally required to pause collection activities, diminishing your leverage.

Use Certified Mail with Return Receipt

Always send your debt validation letter via certified mail with return receipt requested. This costs a few extra dollars but provides undeniable proof that the collector received your request and when they received it. This documentation becomes crucial if you later need to prove the collector violated your rights.

Keep Copies of Everything

Maintain a complete file including copies of your debt validation letter, the certified mail receipt, the return receipt when it arrives, the original collection notice, and any responses from the collector. Organize these documents chronologically to create a clear timeline of events.

Avoid Acknowledging the Debt

In your debt validation letter, don't admit the debt is yours or make any statements that could be construed as acknowledgment. Simply request validation without taking a position on whether you owe the money. Acknowledging a debt can restart the statute of limitations in some states.

Be Specific but Concise

Your debt validation letter should be thorough in listing what documentation you require, but avoid unnecessary elaboration or emotional language. Stick to factual requests supported by the FDCPA. A one-page letter is typically sufficient.

Don't Engage in Phone Conversations

If the collector calls after receiving your debt validation letter, politely decline to discuss the matter over the phone and reiterate that all communication should be in writing. Phone conversations leave no paper trail and can lead to misunderstandings or pressure tactics.

Research Your State's Statute of Limitations

Before sending your debt validation letter, research your state's statute of limitations for the type of debt in question. Different states have different timeframes, typically ranging from three to six years. Include a request for proof that the debt is within this timeframe.

Common Pitfalls to Avoid with Your Debt Validation Letter

Understanding what not to do is equally important for protecting your interests.

Many consumers make the mistake of making a partial payment before sending a debt validation letter. Any payment can be interpreted as acknowledgment of the debt and may restart the statute of limitations. Always validate first, negotiate payment later if the debt proves legitimate.

Another common error is missing the 30-day validation window. Mark your calendar immediately upon receiving a collection notice and send your debt validation letter promptly. Waiting until day 29 or 30 is risky because mail delays could push delivery past the deadline.

Some people draft overly aggressive or threatening debt validation letters, thinking this will intimidate collectors. In reality, hostile language can work against you by making the collector less cooperative and potentially escalating the situation. Professional, businesslike communication achieves better results.

Failing to request written communication only is another oversight. Without this explicit request, collectors can continue calling you, which many consumers find stressful and harassing. Your debt validation letter should clearly state your preference for written communication.

Don't assume that silence from the collector means victory. If you haven't received validation or acknowledgment within 30-45 days, send a follow-up letter and consider filing complaints with the Consumer Financial Protection Bureau and your state's attorney general office.

Free Download: Your Debt Validation Letter Template

Take control of your financial rights with our professionally crafted debt validation letter template. This comprehensive document includes all the legally necessary language and requests to help protect you from questionable collection attempts. Our template can save you time while providing confidence that you're properly exercising your rights under federal law. Customize it with your specific situation details, print it, and mail it via certified mail to start the validation process. Your journey toward resolving debt concerns the right way is just one click away.

Frequently Asked Questions About the Debt Validation Letter

Q:How long does a collection agency have to respond to my debt validation letter?

A:The FDCPA doesn't specify an exact timeframe for collectors to provide validation. However, they must cease collection activities immediately upon receiving your request. Most collectors respond within 30 days, but some take longer. If you haven't received a response after 45 days, send a follow-up letter.

Q:Can I send a debt validation letter after the 30-day window?

A:Yes, you can send a debt validation letter at any time. However, the collector's legal obligation to pause collection activities only applies if you send the request within 30 days of their initial notice. After this window, they can continue collection efforts while investigating your request.

Q:What if the collection agency ignores my debt validation letter?

A:If a collector ignores your debt validation letter and continues collection attempts without providing validation, they're violating the FDCPA. Document all collection attempts, file complaints with the Consumer Financial Protection Bureau and your state attorney general, and consider consulting with a consumer rights attorney.

Q:Should I send a debt validation letter even if I think I owe the debt?

A:Yes, sending a debt validation letter is smart even if you believe the debt is yours. The amount might be incorrect, the collector might not have proper authorization, or the statute of limitations might have expired. Validation protects your interests regardless of the debt's legitimacy.

Q:Can debt collectors contact me while my debt validation letter is being processed?

A:If you sent your debt validation letter within 30 days of the initial collection notice, the collector must cease collection activities until they provide validation. They can acknowledge receipt of your request but cannot demand payment or report the debt to credit bureaus during the validation period.

Q:What happens if the debt validation letter reveals the debt is past the statute of limitations?

A:If validation shows the debt is beyond your state's statute of limitations, you have a complete defense against any lawsuit. The debt becomes legally unenforceable, though it technically still exists. You can use this information to negotiate deletion from your credit report or simply refuse to pay.

Q:Do I need to send separate debt validation letters to each collection agency?

A:Yes, if multiple agencies contact you about different debts, send a separate debt validation letter to each one. Even if they're collecting on behalf of the same original creditor, each collector must independently validate the specific debt they're pursuing.

Q:Can a debt validation letter remove items from my credit report?

A:A debt validation letter goes to the collection agency, not credit bureaus. However, if the collector cannot validate the debt, they must stop collection activities and should remove the item from your credit reports. If they don't, you can separately dispute the item with credit bureaus, citing the collector's failure to validate.